CPF LIFE is supposed to be an annuity scheme that provides members with an income for life from their drawdown age (DDA) or when they join the scheme, whichever is later. In any commercial annuity offering, after the principal sums and schedule are mutually agreed upon and established, the drawdown amount is determined and fixed. As good as written in stone.

That's what Vikram Nair, a politician, lawyer and member of the country's governing People's Action Party, was alluding to. In his example, the monthly income of $1,270 is fixed for life.

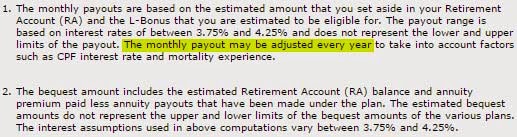

Now look at the fine print on the CPF Life website:

"The payout range is based on interest rates of between 3.75% and 4.25% and does not represent the lower and upper limits of the payout. The monthly payout may be adjusted every year to take into account factors such as CPF interest and mortality experience."

In other words, the people in charge can change their minds, anytime, anyhow. They are telling you in black and white they can adjust the payouts - supposedly based on CPF interest and mortality experience - and damn if they bother about the actuarial science behind the computation, the discipline that applies mathematical and statistical methods to assess risk in insurance, finance and other industries and professions. Actuaries are professionals who are qualified in this field through education and experience. Obviously professionals are not in charge, just the usual set of clowns determined to rip off a docile populace. The Fernvale Lea customers won't be the only ones to start paying closer scrutiny to the fineprint.

Okay, Nair, we need you to explain CPF Life again.

Tattler

*The writer blogs at http://singaporedesk.blogspot.sg/